Growth Creates Pressure Before It Creates Stability

Many businesses encounter their most difficult phase not when sales are low, but when sales begin to grow.

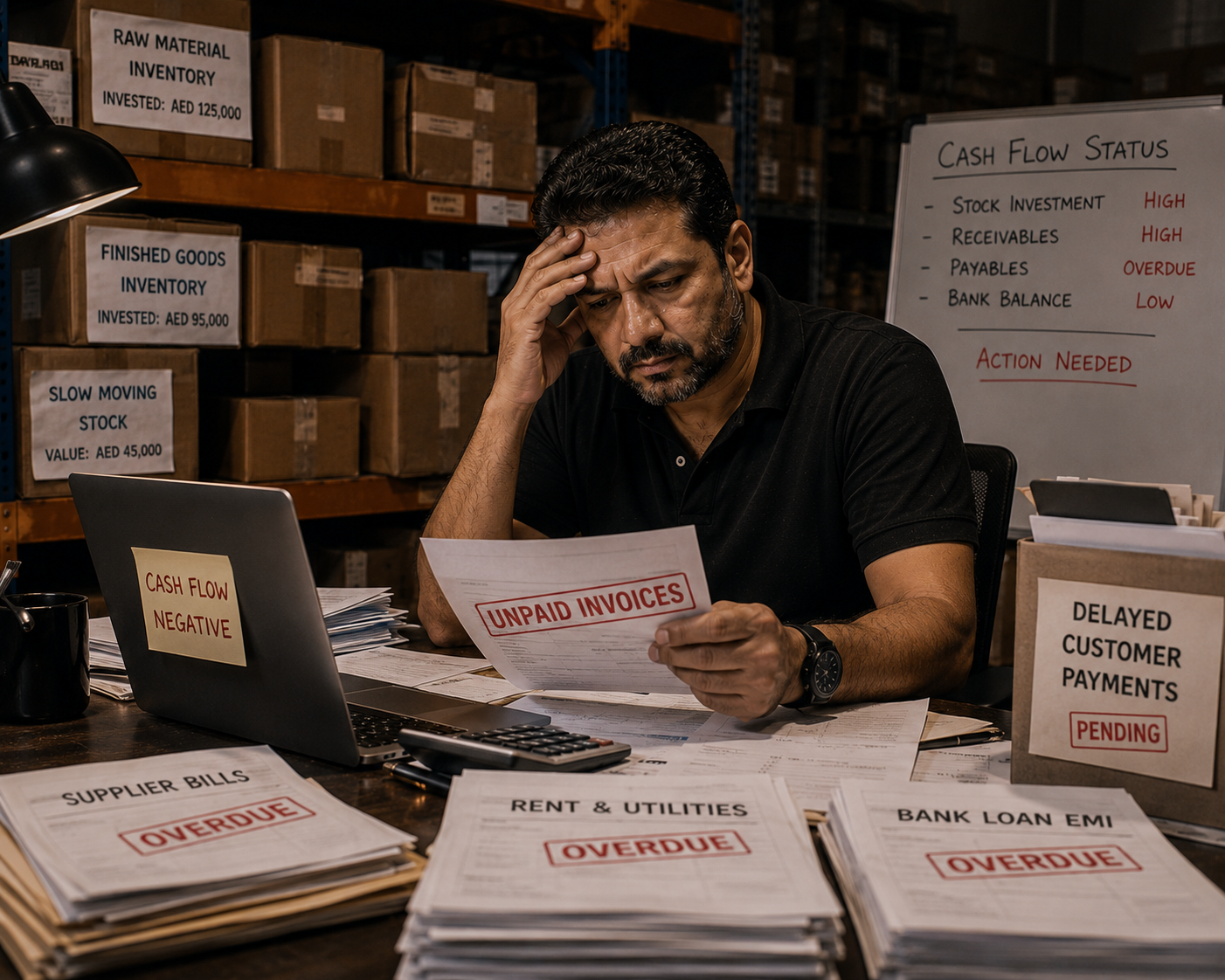

Orders increase, customers expand, and revenue appears to move in the right direction. From the outside, this looks like progress. Internally, however, a different pattern begins to emerge. Cash becomes tight, payments feel delayed, and operational pressure increases.

This situation often feels contradictory. If the business is growing, why does it feel financially strained?

The answer lies in working capital. Growth does not automatically generate financial stability. In many cases, it increases the need for cash before it improves profitability.

What Working Capital Actually Means

Working capital represents the resources a business needs to operate on a daily basis. It is the difference between short-term assets and short-term liabilities.

In practical terms, it answers a simple question:

Can the business continue operating without running out of cash?

Working capital includes:

- inventory (products yet to be sold)

- receivables (money owed by customers)

- payables (money owed to suppliers)

| Component | What It Represents | Impact on Cash |

| Inventory | Unsold goods | Locks cash |

| Receivables | Customer payments pending | Delays inflow |

| Payables | Supplier payments due | Controls outflow |

The balance between these elements determines whether a business has enough liquidity to sustain operations.

Where the Pressure Builds

The challenge with working capital is not its definition—it is how it behaves under real conditions.

A business may sell a product today but receive payment weeks later. At the same time, it must pay suppliers, salaries, and operational expenses on time.

This creates a timing gap.

The Cash Cycle

The working capital cycle can be understood as:

- cash is used to purchase inventory

- inventory is sold

- payment is received later

During this cycle, cash remains tied up. The longer the cycle, the greater the pressure on liquidity.

This is why businesses that appear profitable can still experience financial strain. The issue is not profitability—it is timing.

This dynamic connects closely with cash flow vs profit, where accounting outcomes differ from actual cash availability.

A Simple Scenario: Growth Without Liquidity

Consider a small trading business.

- Monthly sales: $20,000

- Profit margin: 20%

- Expected profit: $4,000

At a glance, the business appears healthy.

But the operational reality is different:

- inventory must be purchased upfront

- customers pay after 30–45 days

- operating expenses are immediate

This means cash is continuously tied up in inventory and receivables.

As sales grow, this requirement increases.

- At $20,000 sales → moderate pressure

- At $40,000 sales → double the working capital requirement

The business grows, but so does the need for cash.

Without sufficient working capital, growth itself becomes a source of strain.

Why Growth Can Create Cash Problems

Growth is often seen as a positive indicator. However, it changes the financial structure of a business.

As sales increase:

- more inventory is required

- receivables increase

- operational costs rise

If these increase faster than cash inflow, the business experiences a cash gap.

This is one of the most common reasons businesses struggle during expansion.

The model works. Demand exists. But the financial structure is not prepared to support the increased activity.

The Hidden Risk: Overtrading

One of the most overlooked risks in business is overtrading.

Overtrading occurs when a business grows faster than its working capital can support. It continues to take orders, expand operations, and increase volume, but does not have enough liquidity to sustain that growth.

This creates a cycle:

- more sales require more cash

- lack of cash limits operations

- operations become inconsistent

Eventually, the business becomes unstable despite strong demand.

Overtrading is not caused by poor sales—it is caused by insufficient financial capacity to support growth.

Working Capital and Pricing Are Connected

Working capital is not only influenced by operations—it is also affected by pricing.

If margins are too low, the business generates less cash per transaction. This reduces the ability to fund inventory, absorb delays, and manage operational costs.

This is why pricing decisions—explored in pricing strategy for small businesses—have a direct impact on working capital.

Higher margins do not just improve profitability; they improve liquidity.

At the same time, pricing must remain aligned with demand. This creates a balance that must be managed carefully.

Managing Working Capital in Practice

Improving working capital does not always require large financial interventions. Often, it involves operational discipline.

Key adjustments include:

- reducing inventory levels without affecting availability

- shortening customer payment cycles

- negotiating better payment terms with suppliers

These changes improve cash flow without altering the core business model.

Practical Example

If a business reduces receivable days from 45 to 30:

- cash is recovered faster

- liquidity improves

- dependency on external funding decreases

Small improvements in timing can have a significant impact on overall financial stability.

The Role of Control and Visibility

Working capital problems often arise not because of lack of profit, but because of lack of visibility.

Many businesses track revenue and expenses but do not closely monitor:

- how long inventory sits unsold

- how long customers take to pay

- when payments are due

Without this visibility, decisions are made based on incomplete information.

Businesses that actively monitor these cycles are better positioned to manage liquidity and avoid unexpected pressure.

Why Early-Stage Businesses Are More Vulnerable

Early-stage businesses face a higher working capital risk because they operate with limited buffers.

- margins are still stabilizing

- demand patterns are uncertain

- access to external funding is limited

At the same time, these businesses often focus heavily on validation and growth—areas covered in how to validate a business idea—without fully accounting for financial structure. (internal link)

This creates a situation where demand is proven, but the business struggles to sustain operations.

Turning Working Capital Into a Decision Tool

Working capital should not be viewed as a constraint—it should be used as a decision-making tool.

Before expanding:

- Can the business support higher inventory?

- Can it absorb delayed payments?

- Can it maintain operations during slower periods?

These questions determine whether growth is sustainable.

A business that grows within its working capital capacity builds stability. A business that grows beyond it creates pressure.

Cash Is Needed Before It Is Earned

One of the most important realities in business is that cash is required before it is earned.

Inventory must be purchased before it is sold. Expenses must be paid before revenue is received.

Working capital bridges this gap.

Businesses that understand this operate with greater control. They plan for timing differences, manage liquidity carefully, and avoid unnecessary risk.

Businesses that ignore it often encounter problems that appear unexpected but are structurally predictable.

Growth Without Liquidity Is Fragile

Growth is often seen as the goal. But growth without liquidity is fragile.

A business can have:

- strong demand

- increasing revenue

- positive margins

and still struggle if working capital is not managed properly.

Sustainable growth is not just about increasing sales—it is about ensuring that the business has the financial capacity to support that growth. Working capital is what makes that possible.