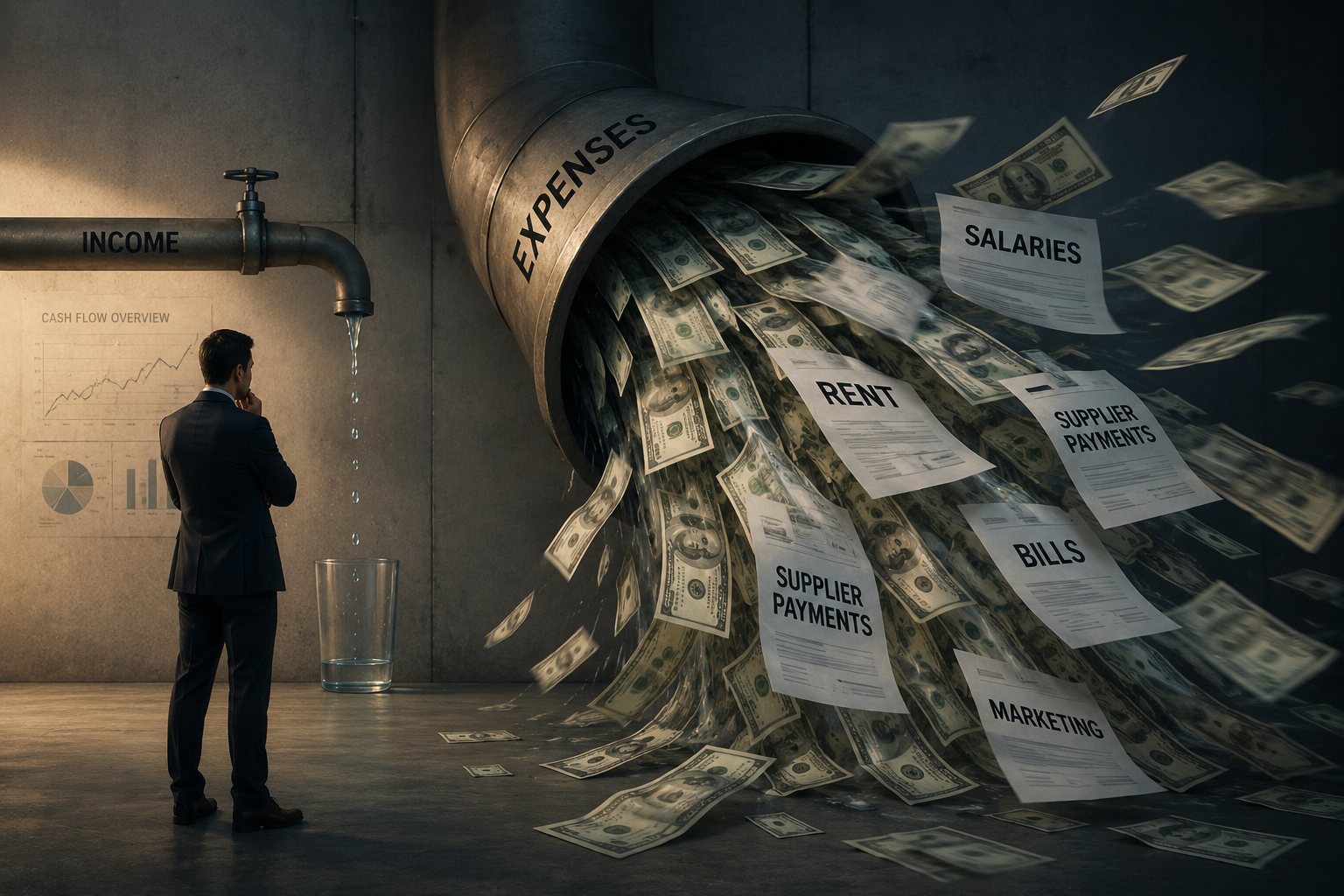

Profit Doesn’t Keep a Business Alive — Cash Does

Many businesses fail at a stage where they appear to be doing well.

Sales are growing. Revenue looks stable. On paper, the business is profitable. Yet, within months, operations begin to strain. Payments are delayed, inventory becomes difficult to manage, and eventually, the business runs out of cash.

At that point, the failure seems sudden. But the underlying issue has been building quietly—often unnoticed.

The assumption that profit equals financial health is one of the most common misunderstandings in business. In reality, profit and cash flow operate differently, and confusing the two can lead to decisions that look correct on paper but fail in execution.

Understanding this difference is not theoretical. It directly affects whether a business survives.

Profit Is an Outcome — Cash Flow Is a Condition

Profit is a calculation. Cash flow is a reality.

Profit measures whether a business earns more than it spends over a period of time. It is derived from accounting principles and includes elements like revenue recognition, expenses, and margins.

Cash flow, on the other hand, tracks the actual movement of money—what comes in and what goes out, and when.

| Metric | What It Represents | Nature |

| Profit | Revenue minus expenses | Accounting-based |

| Cash Flow | Actual money movement | Real-time liquidity |

This distinction becomes critical because profit does not account for timing. A business can record revenue today but receive payment weeks or months later. At the same time, it must still pay rent, salaries, and suppliers on time.

Where the Gap Appears

The gap between profit and cash flow usually appears in operational details. Credit sales, delayed payments, inventory buildup, and upfront costs all create situations where profit exists without corresponding cash.

A business may show strong margins but still struggle to meet immediate financial obligations. This is where many founders encounter problems they did not anticipate.

A Simple Scenario: When Profit Doesn’t Translate to Cash

Consider a small distribution business supplying products to retailers.

The business sells goods worth $5,00,00 in a month with a profit margin of 20%. On paper, that results in $1,00,00 profit. From an accounting perspective, the business appears healthy.

But the reality looks different.

- Retailers are given 30–45 days credit

- Suppliers require payment within 15 days

- Operating costs such as rent and salaries are immediate

This creates a timing mismatch. Money goes out before it comes in.

Even though the business is profitable, it faces a cash shortage. To manage this gap, the owner may:

- delay payments

- take short-term loans

- reduce inventory

Each of these actions introduces new risks. Over time, this pressure accumulates, even though the business continues to show profit on paper.

Why Businesses Collapse Despite Profit

The core issue is not lack of profitability—it is lack of liquidity.

When cash flow is mismanaged, several patterns emerge. Payments begin to pile up. Suppliers tighten credit. Operational flexibility reduces. Eventually, the business becomes constrained not by lack of demand, but by lack of cash.

This problem is often misunderstood because profit creates a sense of security. Founders assume that as long as margins are positive, the business is safe.

In reality, survival depends on the ability to meet obligations on time. Cash flow determines whether a business can continue operating day to day.

This is particularly important in early-stage businesses, where margins are still stabilizing and financial buffers are limited. Many founders focus heavily on validating demand and pricing—areas covered in the validation of a business idea and pricing strategy for small businesses—but underestimate how cash timing affects execution.

Where the Problem Starts: Working Capital

The difference between profit and cash flow is closely tied to working capital.

Working capital represents the money required to run daily operations. It includes inventory, receivables (money owed by customers), and payables (money owed to suppliers).

When working capital is not managed properly, even profitable businesses can run into trouble.

| Component | Impact on Cash |

| Inventory | Locks cash until sold |

| Receivables | Delays cash inflow |

| Payables | Determines cash outflow timing |

If too much cash is tied up in inventory or receivables, the business may struggle to meet immediate expenses. This creates pressure even when the underlying business model is sound.

Understanding this dynamic is essential, especially when scaling. Growth often increases working capital requirements, which means more cash is needed to sustain operations.

The Hidden Risk in Growth

Growth is usually seen as a positive signal. More sales, more customers, and expanding operations all indicate progress.

However, growth can also amplify cash flow problems.

When sales increase, so do:

- inventory requirements

- receivables

- operational costs

If these expand faster than cash inflow, the business can become financially stretched.

This is why some businesses fail during periods of growth rather than decline. The model works, demand exists, but the cash required to sustain that growth is underestimated.

Without careful planning, growth can create the same outcome as poor performance—financial strain and eventual breakdown.

Turning Financial Insight into Better Decisions

Understanding the difference between profit and cash flow is only useful if it changes how decisions are made.

In practice, this means shifting focus from:

- “How much profit are we making?”

to - “When is cash actually coming in and going out?”

This shift affects multiple areas of business:

- Pricing decisions must consider payment cycles

- Credit terms should be aligned with supplier obligations

- Inventory should be managed to avoid unnecessary cash lock-in

It also changes how performance is evaluated. A profitable month is not necessarily a healthy month if cash flow is negative.

Founders who understand this dynamic tend to operate more cautiously and make more sustainable decisions.

Managing Cash Flow in Practice

Improving cash flow does not always require complex financial strategies. Often, it comes down to operational discipline.

Shortening receivable cycles, negotiating better payment terms with suppliers, and maintaining tighter control over inventory can significantly improve liquidity.

At the same time, it is important to build a buffer. Businesses rarely operate in perfectly predictable conditions, and having access to cash provides flexibility when unexpected situations arise.

The goal is not to eliminate risk entirely, but to ensure that the business has enough liquidity to absorb short-term disruptions without affecting long-term viability.

Profit Shows Performance — Cash Flow Determines Survival

Profit remains an important metric. It indicates whether a business model works over time. But it does not determine whether a business can continue operating day to day.

Cash flow does.

A business can survive with low profit for a period of time if cash flow is stable. But it cannot survive without cash, even if profit appears strong.

This distinction is what separates sustainable businesses from those that struggle despite positive numbers on paper. Understanding it early allows founders to avoid one of the most common and preventable causes of business failure.